UFI, the global association of the exhibition industry, has released the latest 31st edition of its flagship Global Exhibition Barometer research, designed to take the pulse of the industry.

The results highlight the recovery of the industry in 2023 in most places around the world.

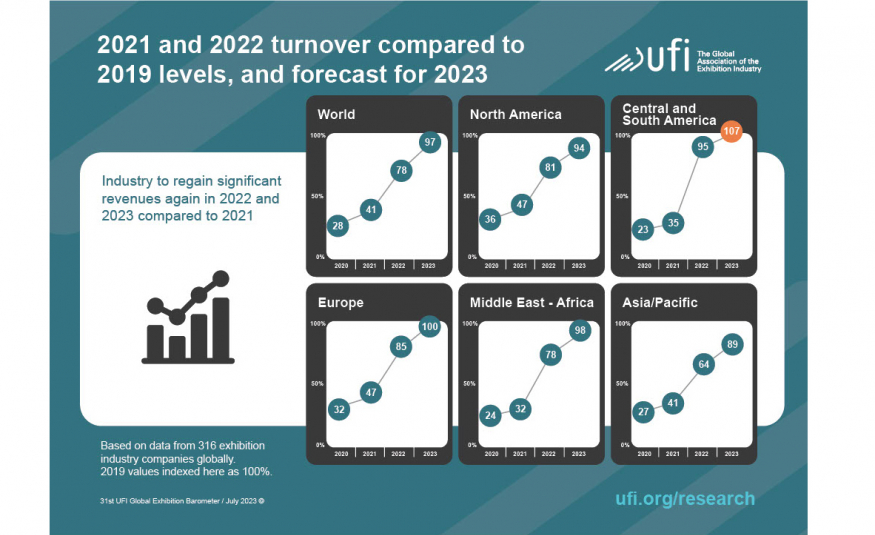

The level of operations is expected to reach 90% for most of the second half of 2023 and several countries expect their 2023 revenues to overcome those of 2019. Globally, the revenues for 2022 and 2023 represent 78% and 97% of the 2019 levels respectively.

More than two-thirds (68%) of companies consider the ‘Changing customer expectations’ as the most impactful element for their business development in the next five years. It is followed with ‘Staffing’, with 54% of answers.

Many business functions are expected to be affected by the development of AI and the main ones are ‘Sales, Marketing and Customer relations’ (62% of respondents), ‘Research & Development’ (58%) and ‘Event production’ (45%), three areas where generative AI applications are being used already by respondents.

“After China’s reopening early this year, the pandemic is now completely in our industry’s rear view mirror, as we are tracking levels of business activities already higher than in 2019 in a growing number of markets. Creating a ‘new normal’ in front of us, the industry is evolving both on digital products and services and on sustainability. New technologies like generative artificial intelligence applications are being explored, while staffing remains a key concern,” says Kai Hattendorf, managing director and CEO at UFI.

Size and scope

This latest edition of UFI’s bi-annual industry survey was concluded in July 2023, and includes data from 351 companies in 61 countries and regions.

The study also includes outlooks and analysis for 19 focus countries and regions – Argentina, Australia, Brazil, China, Colombia, France, Germany, Greece, India, Italy, Malaysia, Mexico, Saudi Arabia, South Africa, Spain, Thailand, the UAE, the UK, and the USA – as well as five additional aggregated regional zones.

Operations

The level of operations has clearly picked up since 2022: the percentage of companies reporting ‘normal activity’ increases from 72% in December 2022 to 79% on average for the first half of 2023.

In parallel, the number of companies reporting ‘reduced activity’ decreased from 20% in December 2022 to 16% in the first half of 2023, to 12% in the second half.

Notably, the countries expected to experience the highest levels of ‘normal activity’ in the second half of 2023 are Australia (97%), the UK (95%), Italy and the USA (94%), Brazil (92%), and Argentina (90%). In China, the expectation of normal activity has risen significantly, with 74% of companies anticipating it compared to only 29% six months ago.

Turnover and operating profits

In terms of operating profits compared to 2019 levels, around half of the companies are declaring an increase or stable level for 2022 and their proportion is increasing to 7 out of 10 for 2023.

Globally, only 2% of respondents expect a loss for 2023, a notable improvement compared to 11% reported for 2022. The highest proportion of companies expecting a loss in 2023 is declared in Germany (11%) and Colombia (10%).

Most important business issues

The most pressing business issue declared in this edition are ‘Internal management challenges’ (21% of answers globally and the main issue in all regions, and most markets). Within ‘Internal management challenges’, 61% of respondents selected ‘Human resource’ issues, 50% selected ‘Business model adjustments’, and 31% selected ‘Finance’. For South Africa and Australia, however, ‘State of the economy in home market’ has become the most pressing issue, for Italy it is ‘Global economic developments’, and for the UK – ‘Impact of digitalisation’ and ‘Sustainability/Climate’.

Overall, the ‘Impact of digitalisation’ comes as the second most important issue globally (17% of answers), followed by ‘Competition with other media’ (15%), ‘State of the economy in home market’ (14%), and then ‘Global economic developments’ comes next (12%, compared to 15% in the previous edition).

The latest results also confirm that the ‘Impact of the Covid-19 pandemic on the business’ is now one of the least pressing issues, globally speaking: only 3% of companies mark it as one of the most important (compared to 11% 12 months ago).

Analysis of the trend around top business issues over the 2016-2023 period identifies several important shifts:

- ‘Impact of digitalisation’ and ‘Competition with other media’ ranks as the main issue, with 32% of answers (compared to 12% in 2016).

- ‘Global economic developments’ and sState of the economy in the home market’ have dropped from being the main issue in 2016 (44% of answers) to 26% in 2023, while the ‘Impact of Covid-19 pandemic on the business’ fell from 29% in 2020 to 3% in 2023.

- And ‘Internal management challenges’ has increased from 13% in 2016 to 21% in 2023.

Key factors for business development

- The 31st Barometer found the following elements were expected to have the greatest impact on their company’s business development in the next five years:

- Globally, ‘Changing customer expectations’ are expected to have the highest impact in the next five years, with 68% of respondents considering it significant. This applies to all regions, except for North America where ‘Staffing’ is the leading answer.

- Approximately 54% of respondents believe that ‘Staffing’ will have a notable impact on business development. Besides North America, it is as well considered to be the key factor in Germany, Australia, and India.

- Around 45% of respondents anticipate that ‘Digitalisation’ will significantly influence business development, it will be especially true in Spain, Argentina, Colombia, and Malaysia.

It is noteworthy that ‘Climate-related regulations’ is expected to be the key factor in France and the UK; and for Italy it will be ‘(De)globalisation’.

Digitalisation

Overall, 64% of respondents have added digital services/products (such as apps, digital advertising, and digital signage) to their existing exhibition offerings. This is especially the case in Europe (67%).

In addition, 55% of respondents globally indicated they have digitised internal processes and workflows (compared to 49% one year ago), and this number is higher in Central and South America (67%).

Overall, 33% reported they have developed a digital transformation strategy for the whole company.

Generative AI applications

The 31st Barometer survey asked a specific question on the impact of generative AI (like ChatGPT). The survey aimed to assess the current utilisation of AI and gauge future expectations.

Globally, the areas expected to be most affected by the development of AI are: Sales, Marketing and Customer Relations (62%), Research & Development (58%) and Event Production (45%). These are precisely the areas where generative AI applications are also mostly used already (22%, 19%, 10% respectively).

Its usage appears to be less prevalent in Europe compared to other regions.

Future exhibition formats

The 31st Barometer sought insights into possible trends that will drive the future format of exhibitions by asking companies to assess four different statements. By using the same question asked in previous editions of the Barometer throughout the pandemic, some useful comparisons can be drawn.

The global results indicate that:

- 91% of respondents (compared to 87% a year ago and 78% two years ago) agree that ‘Covid-19 confirms the value of face-to-face events’ (with 68% stating ‘Yes, for sure’ and 23% stating ‘Most probably’).

- 21% (compared to 31% and 46% previously) believe there will be ‘Fewer international physical exhibitions and, overall, fewer participants’ (with 2% stating ‘Yes, for sure’, 19% stating ‘Most probably’.

- 56% (compared to 61% and 76% previously) believe there is ‘A push towards hybrid events, more digital elements at events’ (with 12% stating ‘Yes, for sure’, 44% stating ‘Most probably’.

- 6% (compared to 6% and 11% previously) agree that ‘Virtual events are replacing physical events’, while 10% are unsure and 84% state ‘Not sure at all’ or ‘Definitely not’.

The 31st Global Barometer survey, concluded in July 2023, provides insights from 351 companies, across 61 countries and regions. It was conducted in collaboration with 31 UFI member associations:

The full results can be downloaded at www.ufi.org/research

The next UFI Global Exhibition Barometer survey will be conducted in January 2024.